Financial Insights

Financial Insights

There’s a version of financial trouble that doesn’t announce itself with a crisis. It doesn’t show up as a single bad month or a shocking invoice. It sneaks in—quietly, persistently—like a slow leak you don’t notice until you’re standing in water.

I call it the Slow Cash Bleed. And it’s one of the most common reasons profitable businesses find themselves short on cash.

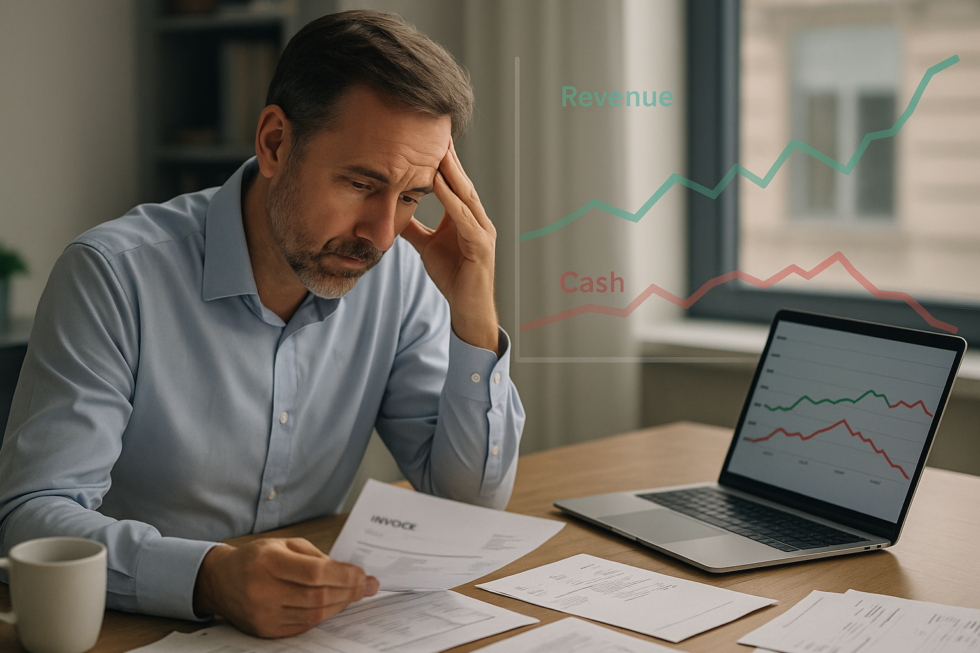

Your P&L says you’re making money. But your bank account tells a different story.

This isn’t a profitability problem. It’s a cash flow timing problem. And the fix starts with understanding where the bleeding is coming from.

Slow receivables. Your customers are taking 45, 60, even 90 days to pay—while your obligations don’t wait. Every day a receivable ages, it’s cash you’re essentially lending out, interest-free.

Inventory creep. You’re holding more stock than you need because you’re afraid of running out. But excess inventory is just cash sitting on a shelf. It’s tied up, not working.

Margin erosion. You’re selling the same volume but at slightly lower margins due to rising costs, discount creep, or customer mix shift. It’s hard to see in the P&L until you run the numbers. Each percentage point of margin is meaningful at scale.

Untracked overhead growth. Subscriptions, staffing, facility costs—these creep up slowly and often go unchallenged because they’re “not that big.” But they compound. Over 12 months, $3K/month in unexamined overhead is $36K you could have kept.

You don’t need a major overhaul. You need visibility. Here’s a simple starting framework:

Then build a 13-week rolling cash flow forecast. It’s not glamorous, but it’s the closest thing to a financial early-warning system I know of.

Most business owners I work with aren’t in trouble because of bad decisions. They’re in trouble because they’ve been operating on feel instead of data. The Slow Cash Bleed is a symptom of that.

When you have clarity—real, current, accurate clarity—you can see the leak before it becomes a flood. You can make decisions from a position of strength instead of reacting to whatever the bank balance says this morning.

That’s the shift. From reactive to proactive. From fog to clarity.

If you’re feeling the Slow Cash Bleed in your business right now, I’d love to help you find it. Let’s schedule a 30-minute Clarity Call and we’ll identify the source together.

Book a free 30-minute Clarity Call. No obligation. No jargon. Just an honest conversation about your business and where financial clarity could take you.

Or call us at (414) 301-9696